Dashline Tools · Free calculator

Dash Cam Insurance Savings Calculator

A dash cam almost never cuts your premium directly. Its real money value appears the day a crash is disputed — when clear footage proves you weren’t at fault. This tool estimates what that’s worth to you.

Currency

Your policy excess

Your annual premium

Your no-claims discount

What your number means

Three things worth quoting

The excess is your money, first

On most claims you pay the excess up front. You get it back only when the other driver’s insurer accepts liability — and footage is how that gets accepted quickly.

One junction can undo years

A single at-fault claim can reset a no-claims discount worth up to 70%. That’s years of built-up savings gone from one disputed moment.

Evidence, not a discount

A dash cam is not a coupon. It’s proof — and proof is what turns a “your word against theirs” claim into a settled, paid one. See the full answer.

How the math works

No black box — here’s the formula

The calculator adds two honest, non-overlapping figures. The at-fault loading is shown as context, not summed, so the total can’t overstate your case.

Total = Excess + ( Premium × No-claims discount% × 2 renewals )

- Excess — the cash you front on a claim. Fully recoverable only if the other side is held liable.

- No-claims setback — losing your discount raises your premium; we count roughly two renewals of that higher cost before it rebuilds.

- At-fault loading (context only) — a separate 20–50% surcharge insurers may add after an at-fault claim. Too variable to total, so it stays out of the headline number.

- Assumptions — UK averages; your policy differs. Cold weather, claim value, age and insurer all move these figures.

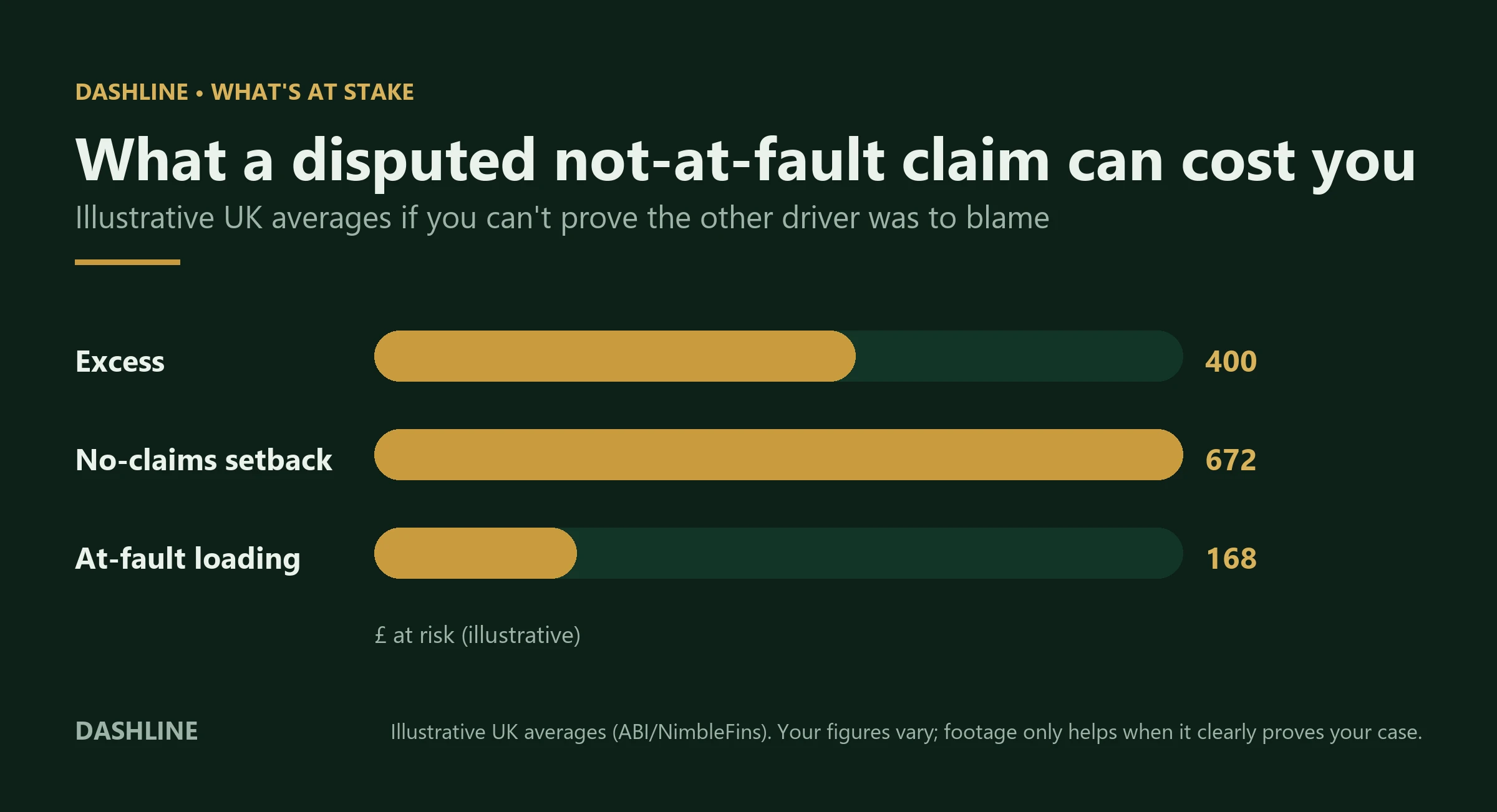

What’s at stake

Where the money goes if you can’t prove it

The default scenario — a £400 excess, a £560 premium and a 60% no-claims discount — puts around a thousand pounds on the line in one disputed junction. Clear footage is what keeps it in your pocket.

The figures behind it

Every number, sourced

| Figure | Typical UK value | Source |

|---|---|---|

| Average total car-insurance excess | £200–£500 | NimbleFins |

| Average annual comprehensive premium | £560 (Q1 2026) | Brumble (ABI data) |

| Maximum no-claims discount | up to 70% (some 75%) | MoneySuperMarket |

| Premium rise after an at-fault claim | +20–50% | Simply Quote |

| Major UK insurers accepting dash-cam footage | all of them | Aviva |

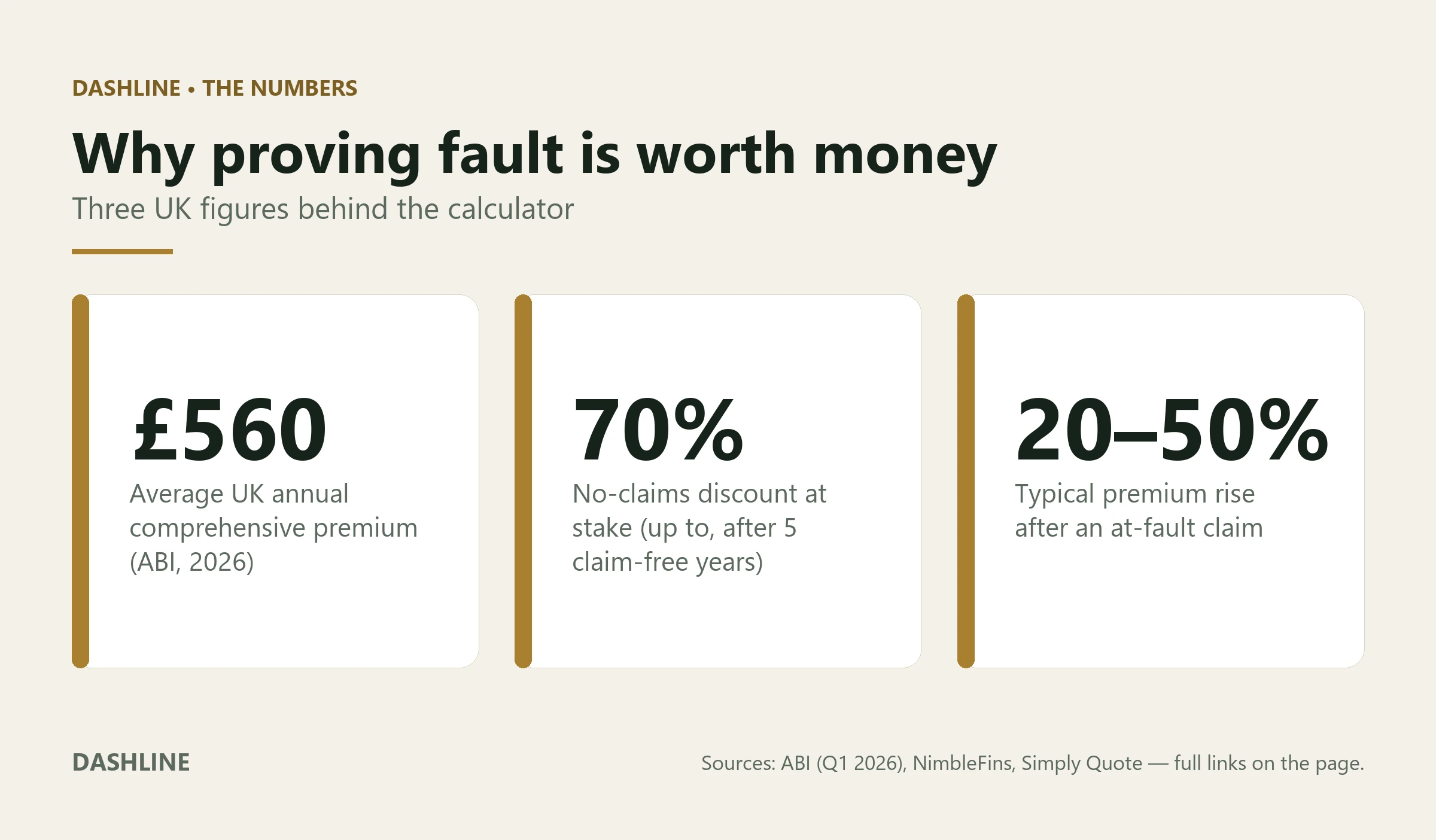

The numbers

Why proving fault is worth money

The honest part

What a dash cam does — and doesn’t do — for insurance

It rarely lowers your premium

A handful of insurers offer up to ~20% off for a dash cam; most offer nothing. Treat any direct discount as a bonus, never the reason to buy.

It only helps if the clip is clear

Speed, angle, light and a clean lens decide whether footage proves anything. A dark, blurred plate settles no dispute.

It protects disputes, not accidents

A camera can’t stop a crash. It changes who gets believed afterwards — and that is where the money is. What to do at the scene.

It works for any car, any insurer

This calculator isn’t Dashline-specific. The math is identical whatever camera records the clip — use your own policy’s numbers.

Use this tool

Cite this page

Found this useful for an article, forum answer or class? You’re welcome to cite it.

Dashline Cameras — “Dash Cam Insurance Savings Calculator.” Retrieved from dashlinecameras.com/dash-cam-insurance-savings-calculator

FAQ

Dash cams & insurance, answered

Does a dash cam lower my car insurance premium?

How does this calculator estimate my saving?

Will insurers actually accept my footage?

Do I get my excess back if I’m not at fault?

Is the calculator only for Dashline owners?

Can a dash cam stop my premium going up at all?

One honest note from us

The camera that records the proof

We built this tool because the honest case for a dash cam is financial, not flashy. If you want a straightforward 4K camera that captures a clear, time-stamped clip — the kind that settles a claim — ours is €85.95, with a screen and memory card included.

View the Dashline 4KFree tool by Dashline Cameras. No sign-up, no data stored — the calculation runs entirely in your browser.

Leave a Reply